Best Cities to Buy vs. Rent in Canada — 2026 (15 Cities Ranked)

By Hami Tahm · Last reviewed May 2026 · 9 min read

★ The 2026 Verdict at a Glance

Best cities to BUY: Regina, Winnipeg, Edmonton, Moncton, Québec City

Best cities to RENT: Toronto, Vancouver, Surrey/GVA, Victoria

Balanced (depends on timeline): Montreal, Calgary, Halifax, Ottawa

The single best predictor: price-to-rent ratio.

Under 20 → buying is competitive. Over 30 → renting is strongly favoured.

Toronto (38+) and Vancouver (35+) are near the top of any global ranking.

Part of our complete rent vs. buy guide for Canada.

Where you live in Canada determines your rent vs. buy answer more than almost any other variable. A first-time buyer in Edmonton has a fundamentally different financial equation than one in Toronto — not because of mortgage rates or personal finances, but because the market itself is built differently.

This ranking uses three data points to assess each city: price-to-rent ratio (home price ÷ annual rent), the monthly cash flow gap between owning and renting, and estimated break-even point. Every city in Canada sits somewhere on this spectrum. Investors comparing rental markets also use cap rate (NOI ÷ property value) alongside P/R ratio.

Jump to:

How We Ranked the Cities

Each city was scored on three factors:

- • Price-to-rent ratio (P/R): Home price ÷ (monthly rent × 12). Under 15 = buying clearly wins. 15–20 = buying competitive. 20–25 = borderline. Over 25 = renting favoured. Over 30 = renting strongly favoured.

- • Monthly cash flow gap: The difference between total monthly ownership cost (mortgage P+I + property tax + insurance + maintenance) and average market rent for a comparable unit. Negative = mortgage is cheaper than rent. Positive = owning costs more per month.

- • Estimated break-even point: The number of years a buyer must stay before the financial benefits of ownership (equity + appreciation) exceed the total transaction costs (LTT + closing + realtor commission on sale).

Data sources: CREA (January 2026), Zoocasa (January 2026), Rentals.ca (March 2026), Ratehub.ca (March 19, 2026), CBC News (March 17, 2026). Mortgage calculations use 3.94% (best 5-yr fixed, March 19, 2026), 20% down, 25-year amortization.

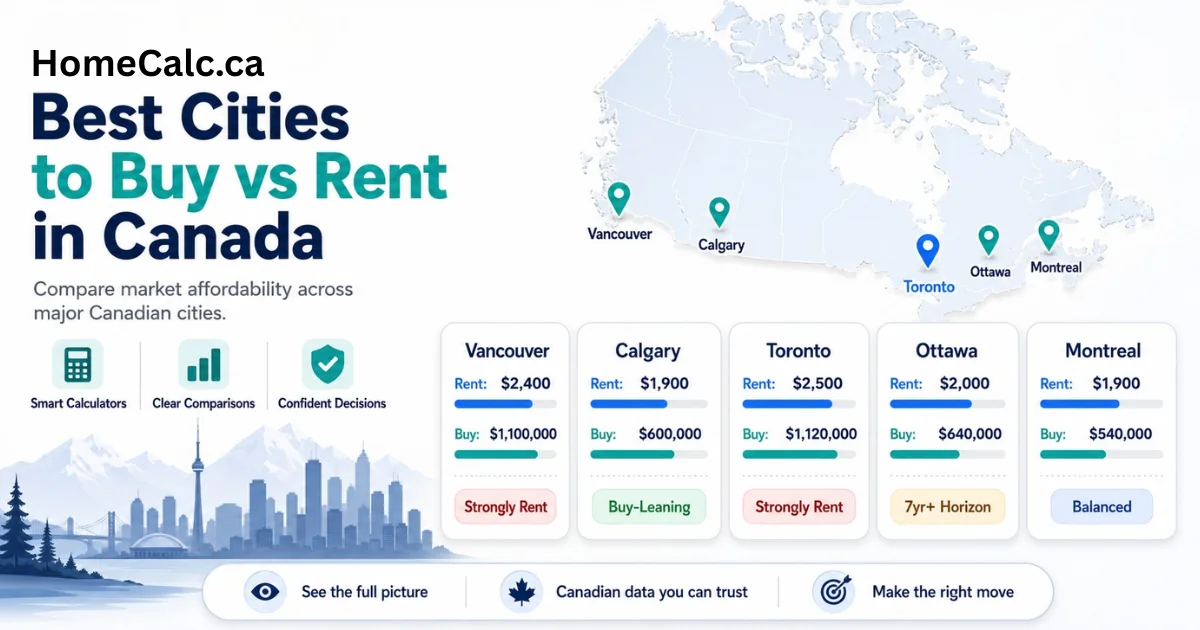

The Master Ranking: 15 Canadian Cities

| City | Avg. Price | Avg. Rent | P/R Ratio | Mo. Gap | Verdict | Recommendation |

|---|---|---|---|---|---|---|

| Regina | $340K | $1,600 | 12–15 | −$107/mo | 🟢 | 🟢 Best to Buy |

| Winnipeg | $350K | $1,600 | 12–14 | −$63/mo | 🟢 | 🟢 Best to Buy |

| Edmonton | $420K | $1,600 | 15–18 | +$244/mo | 🟢 | 🟢 Buy-Leaning |

| Calgary | $600K | $1,900 | 17–19 | +$735/mo | 🟢 | 🟢 Buy-Leaning |

| Halifax | $500K | $1,700 | 17–19 | +$496/mo | 🟢 | 🟢 Buy-Leaning |

| Québec City | $420K | $1,550 | 15–17 | +$400/mo | 🟢 | 🟢 Buy-Leaning |

| Montreal | $540K | $1,900 | 16–19 | +$434/mo | 🟡 | 🟡 Balanced |

| Moncton | $320K | $1,450 | 13–16 | +$200/mo | 🟢 | 🟢 Buy-Leaning |

| Ottawa | $640K | $2,000 | 22–25 | +$810/mo | 🟡 | 🟡 Rent or Buy 7yr+ |

| Hamilton | $720K | $1,950 | 20–23 | +$923/mo | 🟡 | 🟡 Rent or Buy 7yr+ |

| Waterloo | $740K | $1,950 | 21–24 | +$781/mo | 🟡 | 🟡 Rent or Buy 7yr+ |

| Victoria | ~$950,000 | $2,100 | 25–28 | +$1,413/mo | 🔴 | 🔴 Renting Favoured |

| Toronto | $1,120K | $2,500 | 35+ | +$2,420/mo | 🔴 | 🔴 Strongly Rent |

| Vancouver | $1,100K | $2,400 | 38+ | +$2,440/mo | 🔴 | 🔴 Strongly Rent |

| Surrey/GVA | $960K | $2,200 | 30–34 | +$1,957/mo | 🔴 | 🔴 Strongly Rent |

Monthly Gap = total ownership costs minus average rent. Negative = mortgage cheaper than rent. Positive = owning costs more. Data: March 2026.

Best Cities to Buy in 2026

These cities have price-to-rent ratios under 20, monthly ownership costs near or below rent, and break-even points of 3–6 years. Buying makes clear financial sense here.

#1 REGINA — The only major Canadian city where buying is cheaper than renting right now

Avg. home price: $340,000 | Avg. rent: $1,600/month | P/R ratio: 12–15

Monthly mortgage (3.94%, 20% down): $1,493/month — $107 LESS than rent

Break-even: 3–5 years

Regina is the single best buying market in Canada in 2026. The mortgage is already cheaper than rent from day one, the price-to-rent ratio is the lowest of any major Canadian city, and property taxes are among Canada's lowest.

Best for: First-time buyers, value investors, remote workers choosing to relocate out of high-cost markets.

Watch out for: Limited job market diversity; Saskatchewan economy tied to commodity prices (agriculture, oil). Population growth is moderate.

#2 WINNIPEG — Tied with Regina for best monthly cash flow in Canada

Avg. home price: $350,000 | Avg. rent: $1,600/month | P/R ratio: 12–14

Monthly mortgage: $1,537/month — $63 less than rent

Break-even: 3–5 years

Winnipeg is one of only two major Canadian cities where owning costs less per month than renting. It has a more diverse economy than Regina (aerospace, food processing, financial services) and is the 7th largest city in Canada.

Best for: Buyers who want positive monthly cash flow from day one.

Watch out for: Numbeo's 2026 quality of life index ranks Winnipeg among the poorest climates in Canada; the city has below-average safety scores. These lifestyle factors matter beyond the financial math.

#3 EDMONTON — Best major city for buyers who want near-break-even cash flow

Avg. home price: $420,000 | Avg. rent: $1,600/month | P/R ratio: 15–18

Monthly gap: +$244/month (owning costs slightly more)

Break-even: 4–6 years

Edmonton is Canada's most affordable major city for buyers. The monthly gap between owning and renting is just $244 — a figure Zoocasa (January 2026) describes as the smallest premium for ownership of any major Canadian city. Edmonton also benefits from Alberta's 0% provincial income tax.

Best for: Buyers with stable income, first-time buyers with 5–20% down.

Watch out for: Economy closely tied to oil and gas; significant risk in energy downturns. Less diversified than Calgary.

#4 MONCTON — Atlantic Canada's most underrated buying market

Avg. home price: $320,000 | Avg. rent: $1,450/month | P/R ratio: 13–16

Monthly gap: +$200/month (owning costs slightly more)

Break-even: 4–5 years

Moncton is the fastest-growing city in Atlantic Canada and one of the best-value buying markets nationally. Low prices, low transaction costs, bilingual job market (NB's only officially bilingual province), and growing remote worker population.

Best for: Remote workers, bilingual professionals, Atlantic Canada movers.

Watch out for: Limited transit; car-dependent lifestyle. Rent has risen sharply in recent years as demand from remote workers outpaced supply.

#5 QUÉBEC CITY — Best buying market in Ontario/Quebec for francophone buyers

Avg. home price: $420,000 | Avg. rent: $1,550/month | P/R ratio: 15–17

Monthly gap: +$400/month

Break-even: 5–6 years

Québec City consistently ranks among the most affordable provincial capitals in Canada. Home prices have risen modestly (not the explosive growth seen in Ottawa or Halifax), and the local economy is stable (government, tourism, tech). Quebec's low utility costs (hydro rates are among Canada's lowest) reduce total housing costs further.

Best for: Francophone professionals, government employees, families.

Watch out for: French language requirement is a practical barrier for English-dominant buyers; job market narrower than Montreal.

Balanced Markets: Rent or Buy Depending on Your Timeline

These cities have P/R ratios between 16 and 25. Buying is competitive for 7+ year horizons; renting is better for under 5 years. Calgary and Halifax are the most compelling here.

#6 CALGARY — Best buying market in a major Western city (7yr+ horizon)

Avg. home price: $600,000 | Avg. rent: $1,900/month | P/R ratio: 17–19

Monthly gap: +$735/month

Break-even: 6–8 years

Calgary has the most balanced rent vs. buy equation of any major Western Canadian city. The monthly ownership premium ($735) is significant but not extreme, and Calgary's strong long-term appreciation (driven by oil sector and population growth) has historically closed this gap within 6–8 years.

CMHC's chief economist told CBC (March 17, 2026): "Edmonton and Calgary remain the most affordable markets among major Canadian cities."

Best for: Buyers with 7+ year horizon, Alberta professionals, energy sector.

Not for: Anyone likely to move in under 5 years.

#7 HALIFAX — Best coastal buying market in Canada

Avg. home price: $500,000 | Avg. rent: $1,700/month | P/R ratio: 17–19

Monthly gap: +$496/month

Break-even: 5–7 years

Halifax has become one of Canada's most expensive rental markets since the pandemic — average rents exceeded $2,200 by end of 2025. But home prices, while rising, remain accessible compared to Toronto and Vancouver. The monthly ownership premium of $496 is manageable, and the 5-year rule largely applies.

Best for: Atlantic Canada professionals, remote workers, military families.

Not for: Buyers who can't commit to 5+ years.

#8 MONTRÉAL — Most balanced major city in Québec

Avg. home price: $540,000 | Avg. rent: $1,900/month | P/R ratio: 16–19

Monthly gap: +$434/month

Break-even: 6–8 years

Montreal's P/R ratio of 16–19 puts it in the buying-competitive zone — similar to Calgary's. However, Quebec's unique market conditions apply: strong tenant protections, a notary system (not a lawyer) for real estate, and the welcome tax (taxe de bienvenue) on purchase, which adds to closing costs.

Best for: Buyers planning 7+ year stays; bilingual professionals.

Not for: Short-term buyers who underestimate Quebec's closing cost structure.

#9 OTTAWA — National capital with a high-but-manageable ownership premium

Avg. home price: $640,000 | Avg. rent: $2,000/month | P/R ratio: 22–25

Monthly gap: +$810/month

Break-even: 8–10 years

Ottawa is Canada's most stable major real estate market — government employment creates steady demand. But the P/R ratio of 22–25 means the ownership premium is real and sustained. Buyers need an 8–10 year horizon to break even in Ottawa.

Best for: Federal government employees, military, long-term settlers.

Not for: 5-year buyers or those uncertain about long-term plans.

Best Cities to Rent in 2026

In these markets, the monthly premium for ownership is so large — and the price-to-rent ratio so extreme — that renting is the clear financial choice for most people, especially those with time horizons under 10 years.

#10 VICTORIA — High costs, beautiful city, strong renting case

Avg. home price: ~$950,000 | Avg. rent: $2,100/month | P/R ratio: 25–28

Monthly gap: +$1,413/month

Break-even: 9–12 years

Victoria combines Vancouver-level costs with lower wages. The monthly premium of ownership over renting is $1,413 — saving renters roughly $17,000/year in cash flow. For buyers who must stay 10+ years and love the city, it can make sense. For everyone else, renting and investing the savings is superior.

#11-12 WATERLOO REGION & HAMILTON — The "value cliff" cities

Avg. home price: $720K–$740K | Monthly gap: +$780–$920/month

P/R ratio: 20–24 | Break-even: 8–10 years

Waterloo and Hamilton sit just above the $650,000 price threshold where, as Zoocasa (January 2026) documented, the mortgage-to-rent gap nearly doubles. These are expensive for buyers but not as extreme as Toronto. Renting is the better short-term choice; buying requires a 7–10 year commitment.

#13 SURREY / GREATER VANCOUVER AREA — Toronto-level costs, smaller city

Avg. home price: ~$960,000 | Monthly gap: +$1,957/month

P/R ratio: 30–34 | Break-even: 11–13 years

Surrey offers lower prices than Vancouver but the P/R ratio still exceeds 30. The monthly premium of $1,957 over equivalent rent means buyers "pay" nearly $24,000/year more than renters. Renting is strongly favoured.

#14 TORONTO — The most extreme rent vs. buy gap of any major inland city

Avg. home price: $1,120,000 | Avg. rent: $2,500/month | P/R ratio: 37+

Monthly gap: +$2,420/month

Break-even: 11–14 years

Toronto's monthly ownership premium of $2,420 means buyers pay $29,000/year more than renters for comparable housing. In 2026, Toronto is still attracting new supply (Purpose-built rental vacancy rate rose to 3.1% in late 2025), giving renters more negotiating power and incentives. For anyone with a horizon under 10 years, renting in Toronto is almost certainly the better financial choice.

First-time buyers specifically: consider Calgary, Edmonton, or Moncton as starter markets before entering Toronto's extreme P/R environment.

#15 VANCOUVER — The highest price-to-rent ratio of any major Canadian city

Avg. home price: $1,100,000 | Avg. rent: $2,400/month | P/R ratio: 38+

Monthly gap: +$2,440/month (highest in Canada)

Break-even: 10–13 years

Vancouver has the highest average asking rents AND the highest home prices in Canada — a dual burden that creates the worst P/R ratio nationally. The $2,440/month ownership premium means renters save nearly $29,000/year compared to buyers. PWL Capital's data (2025) shows renter-investors in Vancouver underperformed homeowners over 2005–2024 — primarily because Vancouver's appreciation was so extreme it outpaced market returns. This is a market where both buying and renting have unusual dynamics.

use our free rent vs. buy calculator

► See Your City's Numbers

use our free rent vs. buy calculator — Run the numbers for your specific city, home price, and rent

full rent vs. buy guide — The complete rent vs. buy guide for Canada 2026

Should I Buy a House in 2026? — Current Canadian housing market: what changed in 2026

Frequently Asked Questions

Disclaimer: Rankings and data are for informational purposes only. Market conditions change rapidly. All calculations use March 2026 data with stated assumptions. Individual results will vary. Always consult a licensed real estate agent, mortgage professional, and financial advisor before making real estate decisions.

Author: Hami Tahm | Canadian Real Estate Market Analysis

Sources: CREA (January 2026) · Zoocasa (January 2026) · Rentals.ca / Urbanation (March 2026) · Ratehub.ca (March 19, 2026) · CBC News / CMHC (March 17, 2026) · Bank of Canada (March 18, 2026) · PWL Capital / Ben Felix (2025) · Numbeo Quality of Life Index (2026) · HouseIndex.ca (January 2026)