Is It Better to Rent or Buy? What Nobody Tells You

By Hami Tahm · Last reviewed May 2026 · 8 min read

★ The Short Answer

Neither is universally better. Renting is better for flexibility, low upfront cost, and short time horizons. Buying is better for long-term stability, equity building, and markets where the price-to-rent ratio is under 20.

The answer changes completely depending on: your city, how long you stay, your down payment, and one number most people never calculate — the opportunity cost of the money you lock up in a down payment.

Read on for the full picture — including the hidden costs both sides conveniently ignore.

Part of our complete rent vs. buy guide for Canada.

Everyone has an opinion on whether it's better to rent or buy — your parents think buying is always the right move, your financially-savvy friend says renting is rational, and the internet gives you think pieces pointing in every direction. Here's the problem: most of them leave out the parts that don't support their argument.

This post gives you both sides — including the hidden costs that homeownership advocates rarely mention and the wealth-building constraints that renting advocates gloss over. By the end, you'll have the actual math and a clear framework for deciding which option is better for your specific situation.

Jump to:

The Real Math: Renting vs. Buying Side by Side

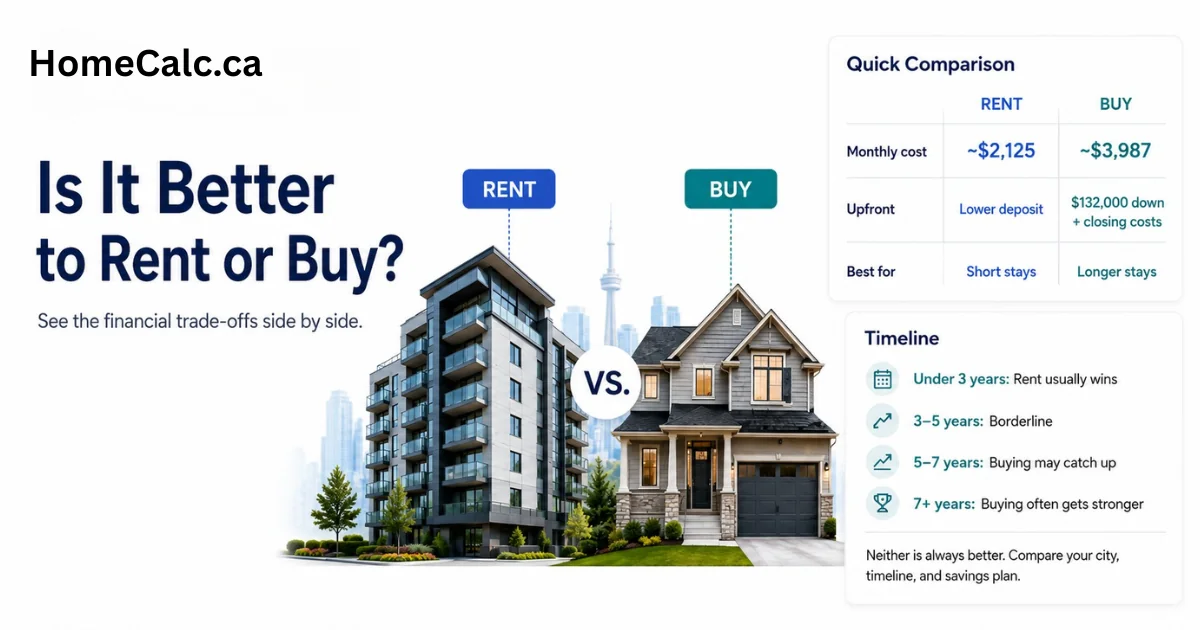

The most important thing to understand: a mortgage payment and rent are not the only costs. The real comparison is total cost of shelter — and on this measure, the gap between renting and buying is much smaller than most people think.

Here's a direct comparison using a typical Canadian scenario in March 2026:

| Buying a $660,000 Home | |

|---|---|

| Down payment (20%) | $132,000 out of pocket |

| Monthly mortgage (3.74%, 25yr) | $2,720/month |

| Property tax (1% avg.) | $550/month |

| Home insurance | $167/month |

| Maintenance (1% rule) | $550/month |

| TOTAL monthly cost (buying) | ~$3,987/month |

| Monthly rent (national avg.) | $2,100/month |

| Renters insurance | $25/month |

| TOTAL monthly cost (renting) | ~$2,125/month |

| Monthly gap (buying costs more) | ~$1,862/month |

At first glance, renting wins by nearly $1,900 a month. But this ignores two critical factors that buyers have and renters don't: equity building and home appreciation. That monthly "cost" of ownership includes a portion that becomes a financial asset — your equity. The real comparison is more nuanced.

★ The Equity Adjustment — What Makes Buying Competitive

On a $660,000 home with 20% down at 3.74% (25yr), in year 1:

• Monthly mortgage payment: $2,720

• Portion going to interest: ~$1,572

• Portion going to principal (equity): ~$1,148

So the true "cost" of the mortgage in year 1 is $1,572/month (interest only), not $2,720 — the rest builds equity. Add home appreciation of 3%/year ($1,650/month on a $660K home) and the owner is building ~$2,800/month in equity + appreciation — money a renter never accumulates.

The question is: does this offset the $1,862/month gap? The answer depends entirely on how long you stay and what you do with the money you save by renting.

The Hidden Costs of Buying (That Nobody Talks About)

Homeownership advocates focus on the mortgage payment and equity. They rarely mention these:

1. Transaction Costs: The Money That Disappears Immediately

Buying and selling a home is expensive. These costs are paid in full upfront and never recovered:

- Land Transfer Tax: 0.5–2.0% of purchase price. In Toronto: double (provincial + municipal LTT). On a $660,000 Toronto purchase: up to $19,950 in LTT alone.

- Closing costs: Legal fees ($1,500–$2,500), home inspection ($400–$600), title insurance ($200–$400), mortgage appraisal ($300–$500). Total: $2,500–$4,000.

- Realtor commission when you sell: 3–5% of sale price. On a $660,000 home: $19,800–$33,000. This is often the biggest financial cost of homeownership that buyers never think about when buying.

Total transaction cost to buy and sell a $660,000 home: $42,000–$57,000 in Toronto. This money is gone — it earns no equity and builds no wealth. You need appreciation and equity to exceed this amount just to break even.

2. The Maintenance Reality Check

The 1% rule says homeowners should budget 1–2% of home value per year for maintenance. On a $660,000 home:

- Year 1–3: Minor expenses (paint, fixtures, appliance repairs): $3,000–$6,000/year

- Year 5–10: Major systems begin to need attention: HVAC ($5,000–$12,000), roof ($8,000–$20,000), windows ($5,000–$15,000), plumbing repairs

- Year 10–20: Kitchen/bathroom renovations if you want to maintain resale value: $20,000–$60,000

Over 10 years: $66,000–$132,000 in maintenance on a $660,000 home. This money is a pure cost — not an investment, not equity.

3. The Opportunity Cost of the Down Payment

This is the most important hidden cost — and the one that homeownership advocates never mention. Your $132,000 down payment isn't free. It's capital that could be invested.

$132,000 invested in a diversified index fund at the S&P/TSX 30-year average of 7% per year becomes $259,813 in 10 years. That's $127,813 in growth that renters can capture — and homeowners cannot, because their capital is locked in brick and mortar.

This doesn't mean renting automatically wins — it means the question is not "mortgage vs. rent" but "home appreciation vs. market returns." In cities where homes appreciate at 5%+/year, buying wins. In cities where appreciation is 2–3%, the market often wins.

The Hidden Costs of Renting (That Nobody Talks About)

Renting advocates focus on flexibility and avoiding maintenance. They rarely mention these:

1. Rent Increases Are Compounding and Relentless

Your mortgage payment (if fixed-rate) is locked in for the term. Your rent is not. In provinces without strong rent control — Alberta, Saskatchewan, Nova Scotia — landlords can increase rent to market rates between tenancies. Even in Ontario and BC, which have annual caps (2.5% in Ontario 2026, 2.3% in BC 2026), long-term renters face a compounding problem. Use our rent-increase guideline calculator to model your local rules:

- At 2.5% annual increase, $2,100/month becomes $2,686/month in 10 years

- At 3% annual increase, $2,100/month becomes $2,822/month in 10 years

- If you move to a new unit in a rent-decontrolled market, you face full market price resets

A fixed-rate mortgage, by contrast, has the same P+I payment from year 1 to year 25. This predictability has enormous long-term value that renters underestimate.

2. You're Building Someone Else's Equity

Yes, your rent is not 'thrown away' — you're paying for housing, a real service. But your landlord is using your rent payments to pay down their mortgage. Every $2,100 you pay in rent is $2,100 that doesn't build your net worth.

Over 10 years at $2,100/month (with 2.5% annual increases), you'll pay approximately $283,000 in rent. That money is gone. A homeowner, over that same period, will have paid roughly $330,000 in mortgage payments — but a meaningful portion of that returned as equity.

3. Renters Rarely Invest the Difference

The 'rent and invest the difference' strategy only works if you actually invest the difference. Most renters don't.

A 2023 Morningstar Canada study found that while renting is mathematically superior in many high-cost markets, renters who pocket the savings from renting over buying rarely invest the difference consistently. A mortgage acts as forced savings — it builds equity whether you're disciplined or not. Renters who lack investment discipline often end up with less wealth than homeowners over 20+ year periods, even in markets where the pure math favoured renting.

4. Security and Stability Risk

In Canada, landlords can end a tenancy for owner's own use, renovations ('renovictions'), or sale of the property. Even with provincial protections, renters face genuine displacement risk — especially in Ontario and BC where these notices are common. Being forced to move disrupts your life, exposes you to full market-rate rents in a new unit, and can make it harder to maintain school districts, community ties, and routines.

is renting really wasting money

The 3 Things That Actually Determine Which Is Better for You

Stop reading national averages. These three variables determine your personal answer.

🔑 Variable 1: How Long You Plan to Stay

Under 3 years: Renting almost always wins. Transaction costs alone destroy any financial advantage from buying.

3–5 years: Borderline. Depends on your market's appreciation rate.

5–7 years: Most markets start favouring buying. Equity catches up to rent savings.

7+ years: Buying is financially competitive or superior in most Canadian markets.

10+ years: Buying wins in virtually every Canadian market except extreme P/R ratios.

Source: BestRates.ca rent vs. buy analysis, 2026; HomeCalc calculator data

🔑 Variable 2: Your City's Price-to-Rent Ratio

Formula: Home price ÷ (monthly rent × 12)

Toronto: $1,120,000 ÷ ($2,500 × 12) = 37.3 → Renting strongly favoured

Vancouver: $1,100,000 ÷ ($2,400 × 12) = 38.2 → Renting strongly favoured

Ottawa: $640,000 ÷ ($2,000 × 12) = 26.7 → Renting slightly favoured

Calgary: $600,000 ÷ ($1,900 × 12) = 26.3 → Borderline / balanced

Halifax: $500,000 ÷ ($1,700 × 12) = 24.5 → Borderline / balanced

Edmonton: $420,000 ÷ ($1,600 × 12) = 21.9 → Buying starts to make sense

Regina: $340,000 ÷ ($1,350 × 12) = 21.0 → Buying makes sense

Under 15: Buying clearly wins | 15–20: Competitive | Over 20: Renting favoured

Note: March 2026 prices and rents. Ratios shift with market conditions.

🔑 Variable 3: What You Do With the Money You Don't Spend

This is the wildcard that changes everything.

If you rent and INVEST the difference (down payment + monthly savings):

→ Renting is financially competitive or superior in most markets

→ Especially true in Toronto and Vancouver where the monthly gap is $1,500–$2,000+

If you rent and SPEND the difference (lifestyle inflation, consumption):

→ Buying is almost always the better long-term wealth-building strategy

→ A mortgage is forced savings. Most renters don't replicate this discipline.

Honest assessment: Research consistently shows most renters do NOT systematically invest the difference. If that's you, buying may build more wealth over 20+ years — even in high-cost markets.

The "Is Renting Throwing Money Away?" Myth — Debunked

"Renting is throwing money away" is one of the most repeated — and most misleading — pieces of financial advice in Canada. Here's why it's wrong. And here's why it's not entirely wrong either.

Why "throwing money away" is wrong

Rent is not wasted — it's payment for housing, a service. A renter gets: a place to live, zero maintenance responsibility, flexibility to move, no exposure to market downturns, and preserved capital that can be invested.

Homeowners also 'throw away' money: mortgage interest (in year 1, roughly 58% of each payment is interest), property taxes (100% sunk cost), home insurance (100% sunk cost), maintenance (100% sunk cost), land transfer taxes (100% sunk cost), realtor commissions (100% sunk cost). On a $660,000 home, a homeowner 'throws away' approximately $42,000–$60,000 in pure costs in the first three years alone.

Why it's not entirely wrong

The grain of truth: a mortgage is forced savings. Every payment builds equity in an asset that has historically appreciated. Most renters, despite the mathematical advantage of renting in high-cost markets, end up with less wealth at retirement than homeowners — because they don't invest the difference.

The Morningstar Canada analysis is clear: in pure financial logic, renting often wins in Toronto and Vancouver. But 'behaviorally,' buying wins — because it imposes savings discipline that most people lack on their own.

is renting really wasting money

Who Renting Is Better For — Right Now in Canada

Renting is the financially smarter choice in March 2026 if you fit this profile:

✓ Renting is better for you if:

• You're in Toronto or Vancouver — price-to-rent ratios exceed 35, meaning you'd pay 35 years of rent to buy the property. The financial math strongly favours renting.

• You plan to move within 5 years — transaction costs alone (LTT + closing + realtor commission) will wipe out any equity or appreciation gains on a short timeline.

• Your income is variable or uncertain — a 25-year mortgage with no flexibility is dangerous if your income can fluctuate by 30%+ in a bad year.

• You don't have 20% down saved yet — CMHC insurance (2.8–4.0% added to your mortgage) and the lack of equity buffer make buying with less than 10% down a significant financial risk in a flat or declining market.

• You're in a career transition or expecting a major life change — new city, new relationship, growing family. Flexibility has real financial value that doesn't show up in any calculator.

• You will actually invest the difference — if you have the discipline to invest the down payment and monthly savings from renting, the math often favours you.

Who Buying Is Better For — Right Now in Canada

Buying is the better choice in March 2026 if you fit this profile:

✓ Buying is better for you if:

• You're in Calgary, Edmonton, Halifax, Regina, or a mid-sized Canadian city — price-to-rent ratios of 15–22 make buying financially competitive even at current rates. Break-even arrives in 5–7 years.

• You plan to stay 7+ years — the break-even point in most Canadian markets is 5–8 years. Long-term buyers capture the full compounding of equity and appreciation while their fixed-rate mortgage stays flat as rent keeps rising.

• You have 20% down and an emergency fund — you avoid CMHC insurance, you start with real equity, and you have a buffer for the maintenance costs that hit every homeowner eventually.

• Your income is stable — fixed mortgage payments are manageable when income is predictable. Two-income households with secure employment are the ideal profile for 2026 buying.

• You value stability and permanence — the ability to renovate, put down roots, and never worry about a landlord ending your tenancy has genuine value beyond the financial math. If this matters to you, it's a valid reason to buy.

• You won't invest the difference if you rent — if you're honest with yourself that the down payment would sit in a savings account earning 3%, a mortgage might be the better forced-savings vehicle over a 20-year horizon.

► See Which Is Better for Your Specific Numbers

use our free rent vs. buy calculator — enter your city, rent, and home price

Frequently Asked Questions

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, mortgage, or legal advice. Market data is as of March 19, 2026. Always consult a licensed mortgage professional or financial advisor before making real estate decisions.

Author: Hami Tahm | Canadian Real Estate & Personal Finance

Sources: Morningstar Canada · CMHC Housing Market Outlook (2026) · CREA (January 2026) · BestRates.ca (March 2026) · WOWA.ca (March 2026) · Bank of Canada (March 18, 2026) · RE/MAX Canada · CPA Canada · HouseIndex.ca