How to Calculate Capital Gains in Canada: Step by Step

By Hami Tahm · Last reviewed July 2026 · 11 min read

⚠️ Tax rules change

Tax rules change. This page reflects Canadian tax rules as of July 2026. Verify current CRA or provincial guidance, or consult a licensed tax professional, before filing or making a financial decision. Source: Canada Revenue Agency

How do you calculate capital gains tax in Canada?

To determine capital gains tax in Canada: (1) calculate your adjusted cost base — purchase price plus acquisition costs plus capital improvements; (2) subtract your ACB and selling costs from your sale price; (3) multiply the resulting gain by the 50% inclusion rate; (4) multiply your taxable capital gain by your combined marginal tax rate. Use the HomeCalc capital gains tax calculator for a province-specific estimate.

Key Takeaways

- Your adjusted cost base (ACB) = purchase price + acquisition costs + capital improvements — every dollar added to your ACB reduces your capital gain dollar-for-dollar.

- Canada's capital gains inclusion rate is 50% for all individuals as of July 2026 — the proposed 66.67% rate above $250,000 was cancelled by the Government of Canada on March 21, 2025.

- Capital gain = sale price minus ACB minus selling costs; taxable capital gain = capital gain × 50%; tax owing = taxable capital gain × your marginal rate.

- The principal residence exemption eliminates capital gains tax on a home for each year it was your principal residence — but you must still report the sale to CRA on Schedule 3.

- The CRA anti-flipping rule (effective January 1, 2023) reclassifies profit from properties sold within 12 months as 100% business income — not a capital gain — unless specific life-event exceptions apply.

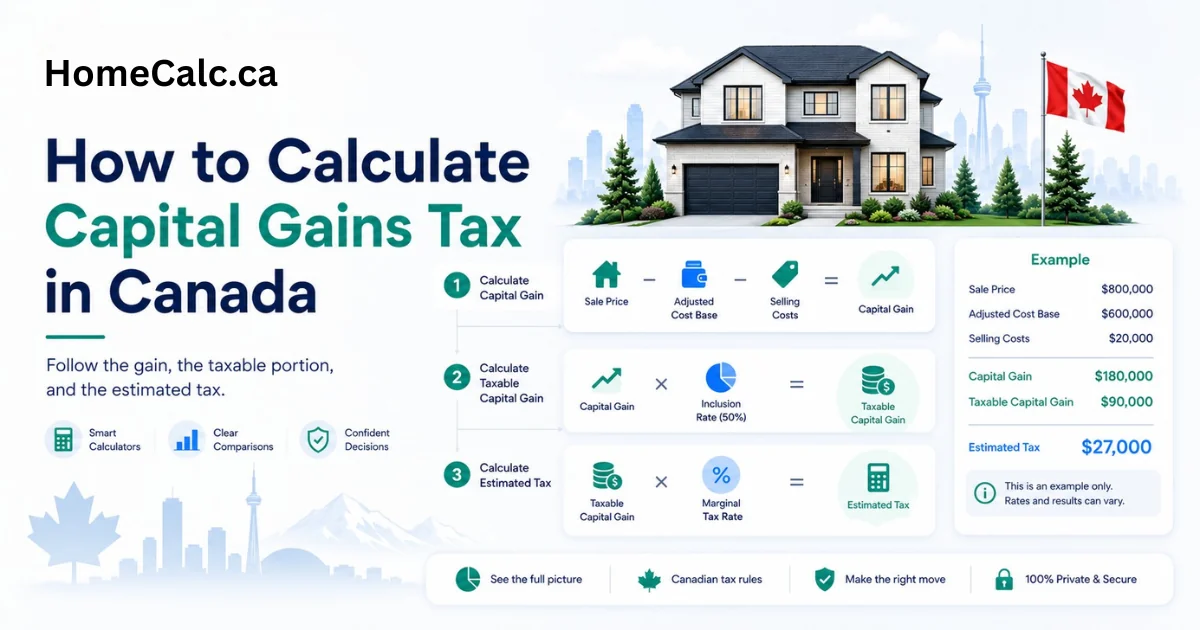

How to Calculate Capital Gains Tax: 4 Steps

Step 1 — Calculate your adjusted cost base (ACB)

Your adjusted cost base (ACB) is the starting point for every capital gains calculation. ACB equals the original purchase price of the asset plus any acquisition costs — legal fees, land transfer tax, home inspection — plus the cost of capital improvements you made while you owned it. For a property bought for $500,000 with $15,000 in acquisition costs and $35,000 in renovations, your ACB is $550,000.

Step 2 — Subtract your ACB and selling costs from your sale price

Subtract your ACB and all selling costs from your sale price to find your capital gain. Selling costs include real estate commissions, legal fees, and any other costs directly related to the sale. If you sell the same property for $870,000 with $20,000 in selling costs, your net proceeds are $850,000. Capital gain = $850,000 − $550,000 = $300,000.

Step 3 — Apply the capital gains inclusion rate

Multiply your capital gain by the capital gains inclusion rate to find your taxable capital gain. In Canada as of July 2026, the inclusion rate is 50% for all capital gains — the proposed 66.67% rate above $250,000 was cancelled by the Government of Canada on March 21, 2025. Taxable capital gain = $300,000 × 50% = $150,000.

Step 4 — Multiply your taxable capital gain by your marginal tax rate

Multiply your taxable capital gain by your combined federal and provincial marginal tax rate. Tax rates vary by province and your total income for the year. An Ontario resident earning $120,000 in employment income plus a $300,000 capital gain faces a combined marginal rate of approximately 43.16% on the taxable portion. Estimated tax = $150,000 × 43.16% = $64,740.

What Counts as a Capital Gain in Canada?

A capital gain in Canada arises when you sell a capital property — such as real estate, stocks, or business assets — for more than your adjusted cost base. The gain is the difference between your net sale proceeds and your ACB. Only 50% of the gain is included in your taxable income under the capital gains inclusion rate.

Determining capital gains tax in Canada requires four steps: calculate your adjusted cost base, subtract it and selling costs from your sale price, multiply the resulting gain by the 50% inclusion rate, and apply your combined federal and provincial marginal tax rate.

Capital properties include real estate (other than your qualifying principal residence), publicly traded stocks and ETFs, mutual fund units, business assets, and certain other investments. Personal-use property — furniture, a car — is generally not subject to capital gains tax unless it is "listed personal property" such as artwork or jewellery with significant value.

CRA requires you to report capital gains on Schedule 3 of your T1 personal income tax return for the year in which you sell the property — even if the gain is fully sheltered by the principal residence exemption. Failure to report can result in CRA denying the exemption. CRA capital gains overview.

Step 1 — Calculate Your Adjusted Cost Base (ACB)

Your adjusted cost base (ACB) is the total amount you invested in a property, including its purchase price, acquisition costs (legal fees, land transfer tax, home inspection), and capital improvements made during ownership. ACB is your baseline for determining capital gains — every dollar added to your ACB reduces your taxable gain. Keep all receipts for improvements; CRA may request documentation.

What to Include in Your ACB

Your adjusted cost base in Canada equals your original purchase price plus acquisition costs (legal fees, land transfer tax, home inspection) plus capital improvements made during your ownership.

Acquisition costs that can be added to ACB: legal fees paid on purchase, land transfer tax, home inspection fees, real estate commission paid by the buyer at purchase, and title insurance. These costs are often overlooked — on a $500,000 purchase they can easily total $15,000–$20,000, reducing a future capital gain by the same amount.

| ACB Component | Definition | Example Amount |

|---|---|---|

| Purchase price | What you paid for the property | $500,000 |

| Acquisition costs | Legal fees, land transfer tax, home inspection, real estate commission at purchase | $15,000 |

| Capital improvements | Additions, renovations that increase value or extend useful life (NOT routine maintenance) | $35,000 |

| Total ACB | Sum of all components above | $550,000 |

| Note | Regular maintenance and repairs are NOT added to ACB | — |

Source: Canada Revenue Agency — Calculating your capital gain or loss (canada.ca)

Capital Improvements That Increase Your ACB

A capital improvement is work that adds value to the property, adapts it to a new use, or extends its useful life. Examples: adding a new bathroom, finishing a basement, building a deck, installing a new roof, or replacing windows. These are added to your ACB.

Routine maintenance and repairs — painting, fixing a leaky faucet, replacing broken tiles — are not capital improvements and cannot be added to your ACB. The distinction matters: a $35,000 basement renovation added to your ACB directly reduces your capital gain dollar-for-dollar when you sell. CRA capital gain calculation formula.

Step 2 — Calculate Your Capital Gain and Apply the Inclusion Rate

Your capital gain equals your net sale proceeds minus your ACB. Net proceeds are your sale price less selling costs — real estate commissions, legal fees, and other direct selling expenses. Multiply the resulting capital gain by the 50% inclusion rate to find your taxable capital gain. In Canada as of July 2026, 50% of every dollar of capital gain is added to your income for the year.

The 50% Capital Gains Inclusion Rate — How It Works

As of April 2026, Canada's capital gains inclusion rate is 50% for all individuals — the proposed 66.67% rate above $250,000 was cancelled by the Government of Canada on March 21, 2025 (source: canada.ca). For a full breakdown of the history and legislative status, see Canada's capital gains inclusion rate.

50% Inclusion Rate — Confirmed April 2026

Canada's capital gains inclusion rate is 50% for all individuals as of July 2026. The federal government proposed raising the rate to 66.67% on gains above $250,000 per year in Budget 2024, but cancelled that proposal on March 21, 2025. All content on this page reflects the confirmed 50% rate. Source: Government of Canada — Department of Finance, March 21, 2025.

Proposed 66.67% Rate — Cancelled March 2025

Budget 2024 proposed raising the inclusion rate to 66.67% on capital gains above $250,000 for individuals. That proposal was formally cancelled by the Government of Canada on March 21, 2025. The 50% rate remains in effect for all capital gains for individuals regardless of amount. Do not use tiered inclusion rates when calculating capital gains owing in 2026.

Step 3 — Estimate Your Tax Owing by Province

Multiply your taxable capital gain by your combined federal and provincial marginal tax rate for the year. There is no separate capital gains tax rate in Canada — the taxable portion is added to your total income and taxed at your marginal rate. Rates vary by province and by your total income. An Ontario resident at the 43.16% marginal bracket owes approximately $64,740 on a $300,000 capital gain.

Federal + Provincial Marginal Rates Combined

Canada has no flat capital gains tax rate. Instead, your taxable capital gain is added to your other income for the year and taxed at your combined federal and provincial marginal rate. The combined top marginal rate on capital gains (after 50% inclusion) ranges from approximately 21.6% in Alberta to 26.8% in Nova Scotia, at the highest income bracket. At mid-income levels, effective rates are lower.

The calculation is straightforward: apply the 50% inclusion rate to your capital gain, then tax the resulting taxable capital gain at your marginal rate for the year. The taxable capital gain is added on top of all your other income — it does not get its own separate rate slot.

Worked Example: $300,000 Gain in Ontario

A Canadian taxpayer with a $300,000 capital gain applies the 50% inclusion rate to arrive at a $150,000 taxable capital gain, then multiplies by their combined marginal rate — approximately $64,740 in Ontario at the 43.16% bracket.

| Step | Description | Amount |

|---|---|---|

| Sale price | What the property sold for | $870,000 |

| Less selling costs | Real estate commission + legal fees at sale | ($20,000) |

| Net proceeds | Sale price minus selling costs | $850,000 |

| Less ACB | Purchase price + acquisition costs + improvements | ($550,000) |

| Capital gain | Net proceeds minus ACB | $300,000 |

| Inclusion rate | 50% — confirmed April 2026 | 50% |

| Taxable capital gain | $300,000 × 50% | $150,000 |

| Ontario marginal rate | Combined federal + provincial at ~$120K income + this gain | 43.16% |

| Estimated tax owing | $150,000 × 43.16% | ~$64,740 |

Note: Estimated tax only. Actual amount depends on total income, province, deductions, and applicable credits. Consult a tax professional.

For a province-specific estimate with your actual numbers, use the Canada capital gains tax calculator.

Capital Gains on Real Estate — Three Scenarios

Whether you owe capital gains tax on real estate in Canada depends on how you used the property. Your principal residence is exempt for each year you designated it — but you must report the sale. Investment and rental properties are fully subject to the 50% inclusion rate with no exemption. Properties sold within 12 months may be reclassified as business income under the CRA anti-flipping rule.

Principal Residence — When Capital Gains Are Exempt

The principal residence exemption eliminates capital gains tax in Canada for each year the property was your principal residence, fully exempting a gain if you lived there for every year of ownership — but you must still report the sale to CRA on Schedule 3. For the full eligibility criteria, partial exemption formula, and cottage rules, see the complete guide to principal residence exemption rules.

Principal Residence Exemption — Key Facts

You can designate only one property as your principal residence per year. The exemption eliminates the capital gain for each year of designation — if you owned it for 10 years and designated it for all 10, the gain is fully exempt. Since 2016, you must report the sale on Schedule 3 even if fully exempt. CRA principal residence exemption rules Failure to report can result in CRA denying the exemption.

If you rented the property for part of your ownership period, the exemption applies only to the years it was designated as your principal residence. The capital gain is prorated using the CRA formula: ((years designated + 1) ÷ total years owned) × capital gain = exempt amount. The "+1" accounts for a one-year grace period CRA provides when you purchase a new property.

Investment Property and Rental Real Estate

Capital gains on rental property and investment real estate in Canada are fully subject to the 50% inclusion rate with no principal residence exemption, and CCA recapture may increase your taxable income further in the year of sale.

CCA Recapture — Additional Tax When You Sell a Rental Property

If you claimed capital cost allowance (CCA depreciation) on a rental property, you may owe CCA recapture when you sell — the depreciation you claimed gets added back to your income in the year of sale, on top of any capital gain. CCA recapture is taxed as regular income (100% inclusion), not at the 50% capital gains rate. Use the HomeCalc capital cost allowance calculator to estimate this exposure.

For a full breakdown of tax implications when flipping or selling rental property, see capital gains vs. business income on a flip. For rental income analysis before a sale, the how to calculate cap rate on investment property guide covers NOI and yield.

The CRA Anti-Flipping Rule — When Your Gain Becomes Business Income

Under CRA's anti-flipping rule, effective January 1, 2023, profit from selling a Canadian property held less than 12 months is treated as 100% business income — not a capital gain — unless specific life-event exceptions apply.

⚠️ CRA Anti-Flipping Rule — Effective January 1, 2023

If you sell a residential property within 12 months of buying it, CRA treats the entire profit as business income — 100% taxable, no 50% inclusion rate, no principal residence exemption. Exceptions exist for certain life events: death of a related person, divorce, serious illness or disability, an eligible relocation where the new home is at least 40 km closer to the new work, business, or school location, or insolvency. CRA Schedule 3 capital gains reporting and consult a tax professional before filing.

The 12-month clock starts from the date of closing, not the date of the purchase agreement. The anti-flipping rule applies to residential properties — not to commercial real estate or land. To estimate the tax impact of a flip under the 100% business income treatment, use the house flip tax calculator.

▶ Calculate your capital gains tax — province by province

- Open Capital Gains Tax CalculatorEnter purchase price, improvements, sale price, and province. Applies the confirmed 50% inclusion rate and combined marginal rates for 2026.

Frequently Asked Questions

Sources

- Canada Revenue Agency — Line 12700 — Capital gains overview (Accessed April 2026)

- Canada Revenue Agency — Calculating your capital gain or loss (ACB methodology) (Accessed April 2026)

- Canada Revenue Agency — CRA principal residence exemption rules (Accessed April 2026)

- Canada Revenue Agency — Canada's new anti-flipping tax (January 2023) (Accessed April 2026)